What You Need to Know About Refinancing with an HEI

Have you been thinking about refinancing your home? If you have a home equity investment from Hometap, you might be wondering if it’s even possible to refinance while you have an active Investment. We’re happy to let you know that it is possible as long as your refinance meets Hometap’s guidelines — check out everything you need to know about the process and how to get started below.

If you do plan to settle your Investment with a refinance, that’s a different situation than what we’re explaining below, but don’t worry — we have you covered here.

Why Refinance?

There are several reasons why you might want to refinance, including:

- To secure a lower interest rate and smaller monthly payments

- To shorten your mortgage term

- To move from an adjustable-rate mortgage to a fixed-rate mortgage (or vice versa)

However, no matter why you want to refinance, your lender will probably require Hometap to sign a Subordination Agreement before proceeding.

How Does a Mortgage Subordination Work?

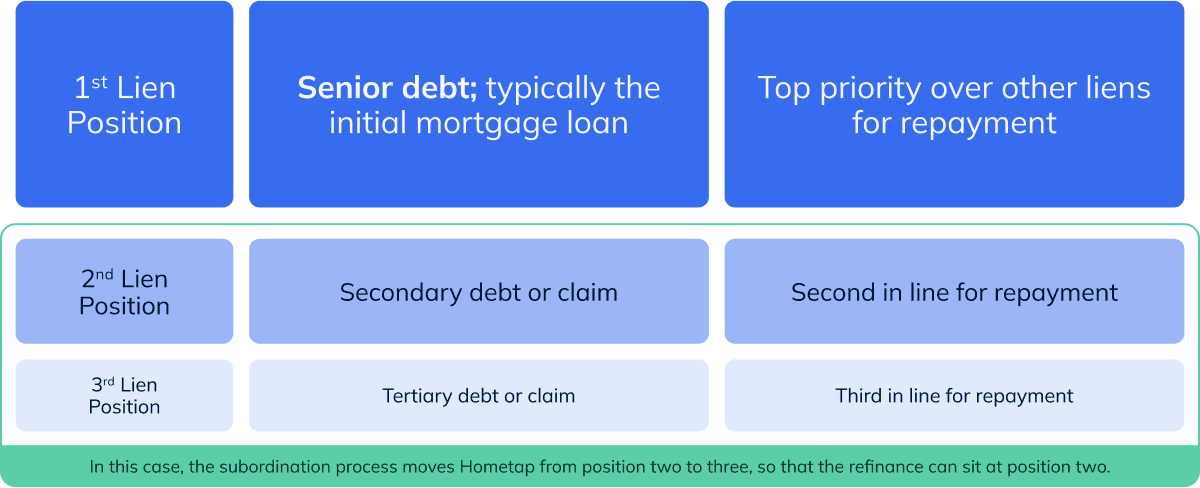

Don’t let the jargon intimidate you. A mortgage subordination is just a process where one mortgage is ranked or prioritized below another mortgage on the same property. This means that if the property is sold or foreclosed upon, the mortgage that was subordinated will be paid off after the one that holds a higher priority. This typically happens when a homeowner wants to take out a second mortgage or home equity loan while keeping their first one. The first mortgage retains its primary position, and the new one becomes secondary, or subordinate, in terms of repayment priority.

How to Let Us Know If You’re Refinancing

If you’re refinancing your mortgage without settling your Investment, the first step is to get in touch with us via homeowners@hometap.com to let us know about your plans prior to initiating the process with your lender, and whether you plan on a cash-out refinance or rate-and-term refinance. A cash-out refinance replaces your existing mortgage with a new, larger loan, allowing you to take out cash, while a rate-and-term refinance replaces your existing mortgage with a new one with a different interest rate or term, without taking out additional cash.

Once you’ve contacted us, a member of the team will respond to you as soon as possible with an email that outlines all of the required documents we’ll need to review. This typically includes:

- 1008 (Underwriting transmittal)

- 1003 (Mortgage application)

- Signed loan estimate

- Closing disclosure

- Title report

- Copy of the physical appraisal

- Lender approval

- Borrower’s authorization (if applicable)

Once we receive the documents, a member of our team will review them and calculate what’s called the owner’s ending equity (OEE) in the property. This allows us to determine whether or not there is enough equity in your property to approve the refinance. Keep in mind that cash-out refinances have different equity than rate-and-term ones.

Here are some additional things to keep in mind as you go through this process:

- Hometap won’t subordinate to lower than 3rd lien position

- The appraisal must be a physical (in-person) lender-ordered appraisal that has been completed within the last 90 days. If you did not get a lender ordered appraisal, Hometap will order one for you from our appraisal management company at your expense. Please note that not all appraisals will be approved for use for purposes of settlement, and we may require one to be performed by our own third-party vendor.

- The new loan cannot contain a balloon payment or negative amortization

- If there is an active default* event on the Investment, this may need to be resolved first

- Depending on the status of your Investment, the approval process can take a couple of weeks

As always, if you have any questions along the way, our Investment Support team is here to help you through the process and answer any questions that you may have! Just reach out to homeowners@hometap.com.

*An active default event is any action taken that violates our Hometap agreement. Examples would be, but are not limited to: inactive insurance policy, delinquent taxes, delinquent senior lien payments, ownership changes, new liens, bankruptcy and/or foreclosure. Section 2 of the Option Purchase Agreement, which can be found in your account, will outline the specifics of a default scenario.

You should know

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

More in “Manage your Investment”

Settling Your Home Equity Investment with a Refinance

Beyond Stability: Why Your Financial Health Matters