The Complete Costs of Buying and Selling a Home

Estimating the all-in costs of purchasing or selling a home can be challenging, especially if either process is new to you. Aside from the list price, there are many potential hidden and/or unexpected costs along the way. And as with most things, there’s a lot of gray area, including the fact that many expenses vary by region or fluctuate with the current market conditions.

Whether you're a first-time homebuyer or an experienced seller, understanding the full spectrum of potential costs and strategies can help you avoid surprises. This guide will walk you through some of the most common expenses that come with buying a home, and since most repeat buyers are likely selling a property at the same time, we’ll also cover those typical costs so that you can better plan for the all-in costs of moving homes. For the sake of easy math, we’ll use $400,000 as the sale price and purchase price of a home in all estimated examples.

Understanding the Costs of Buying a Home

There are more expenses associated with buying a home than the list price. Here's a breakdown of the costs you should anticipate — broken out by upfront costs, ongoing costs, and variable expenses you may need to factor in.

Upfront Costs of Buying a Home

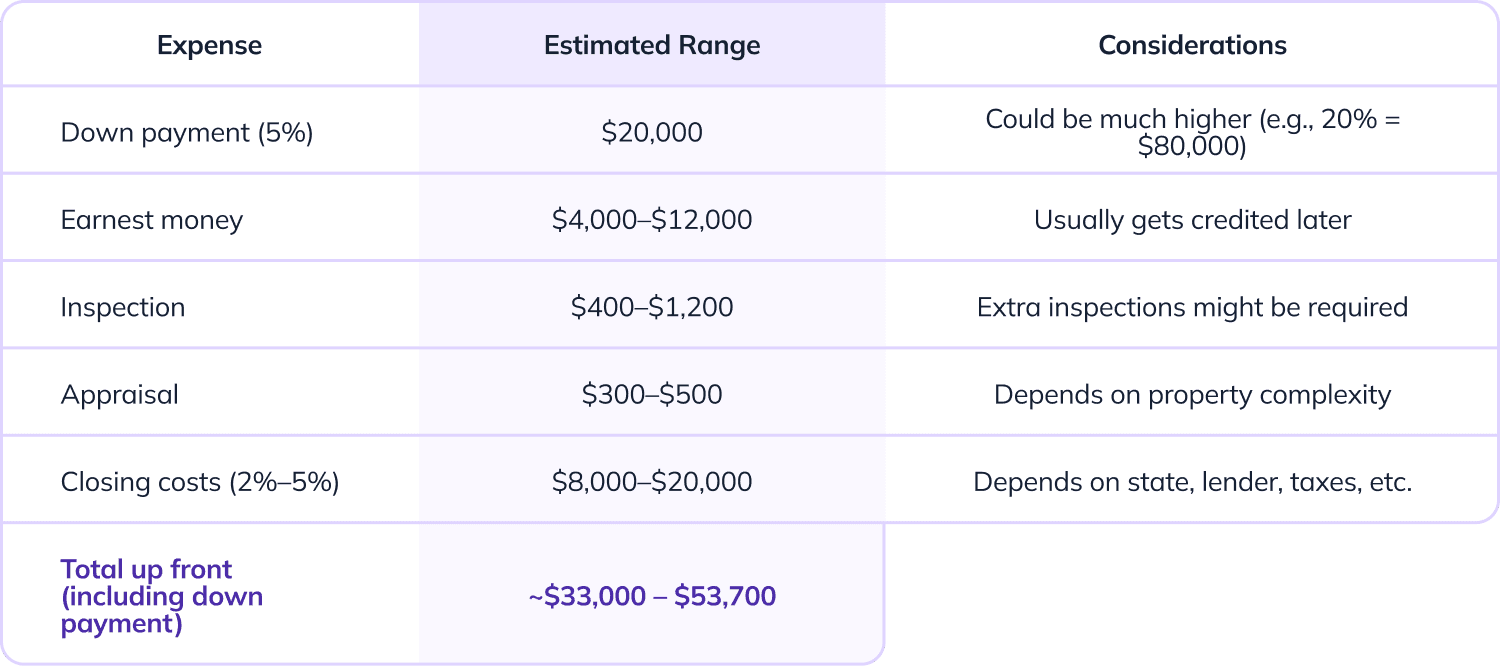

1Down Payment

The down payment is your initial equity contribution. Conventional loans often require 5%–20% of the home price up front, though some government-backed or specialized programs will accept as little as 3% (or even 0% for VA).

The higher your down payment, the lower your mortgage balance, which reduces your interest paid over time.

Lenders may require a larger down payment (or deny certain loan programs) if your credit is weaker or the property is higher risk (e.g., a fixer-upper or non-warrantable condo).

2. Earnest Money (a.k.a. Good Faith Deposit)

To demonstrate serious intent, buyers typically offer what’s called “earnest money,”an amount often equivalent to 1%–3% of the purchase price. This sits in an escrow account and is applied toward the down payment or closing costs.

For instance, for a $400,000 home, earnest money might be $4,000–$12,000. If you cancel the deal within allowed contingencies (such as the inspection), you may get it back; but if you back out without valid reasons, you could forfeit it.

3. Home Inspection Fees

A home inspection can reveal issues with plumbing, electrical, roof, foundation, pests, etc.). Typical costs vary by region and home size, but a general range is $300–$600 for a standard single-family home (1,500-3,000+ sq. ft); for large, older, or complex homes, specialized inspections (e.g., HVAC, mold, radon) may run $100–$400 more per inspection.

4. Appraisal Fees

Lenders require appraisals to verify that the home’s value supports the loan. Costs typically range from $300–$500 but again vary by region and home size, among other factors.

5. Buyer Closing Costs

These expenses can include loan origination, title search and insurance, escrow, recording fees, prepaid taxes, and more. Buyer closing costs often run at 2%–6% of the purchase price. Some lenders or sellers may pay a portion of these fees via concessions, but that usually increases the purchase price or is limited by program rules.

Let’s take a look at what a sample balance sheet could look like for a buyer purchasing a $400,000 home.

Depending on your reason for estimating buying and/or selling costs, it may not make sense for you to factor in ongoing homeownership expenses. However, these costs are frequently overlooked and can take new homeowners by surprise, so it’s important that we don’t gloss over them.

Other Costs to Consider

These are some of the applicable costs that you’ll also want to factor into your bottom line.

1. Mortgage Insurance (PMI/MIP)

If your down payment is less than 20% on a conventional mortgage, you’ll likely need private mortgage insurance (PMI).PMI typically costs 0.3%–1.5% of the original loan annually. So on a $400,000 loan, PMI might range from $1,200–$6,000 per year.FHA loans require mortgage insurance premium (MIP), which can last for the life of the loan if down payment is low.

2. Utilities, Services, & Operating Costs

Ongoing monthly expenses that keep your home running may include water, sewer, electricity, gas, trash, internet, security, and lawn care.Depending on location and house size, these might run $200–$800+ per month.

3. Moving/Relocation Expenses

Moving costs could include:

- Professional movers (truck, labor, packing)

- Moving van or trailer rental

- Packing supplies (boxes, tape, padding, moving blankets)

- Insurance or valuation coverage

- Fuel/travel costs

- Storage (if there’s a gap between move-out and move-in dates)

- Temporary lodging and meals if move spans multiple days

- Time off work

Ongoing Homeowner Expenses

Even after you close on your home and move in, the costs continue. Here’s a more detailed look at some common homeownership expenses.

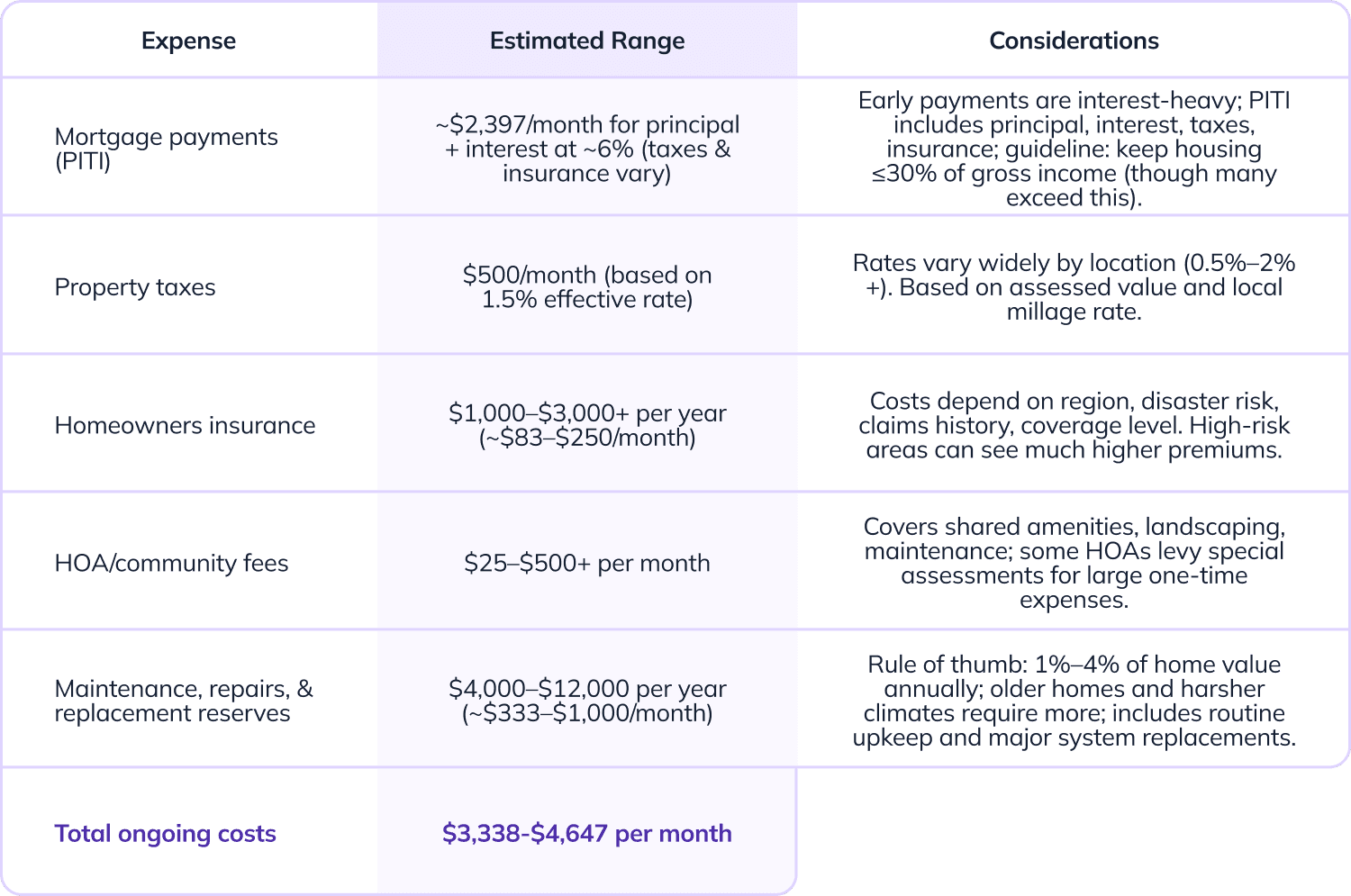

1. Mortgage Payments (PITI)

Your monthly payment typically includes principal, interest, taxes and insurance. You may see this referred to as PITI.

The interest portion in early years is high; as you pay down the principal, more of your payment goes to equity.

For example, with a $400,000 mortgage at ~6% interest over 30 years, the base mortgage (principal + interest) is about $2,397 per month.

A common guideline, originated by the Department of Housing and Urban Development (HUD),is that your total housing costs should stay below 30% of gross monthly income, though in many markets people exceed this.

2. Property Taxes

Property taxes are based on the home’s assessed value and local millage rate. These can vary dramatically by location; rates in some areas may be 0.5%, while others may exceed 2% or more of home value annually. This map illustrates just how widely rates can vary.

If your home is $400,000 and your effective tax rate is 1.5%, that’s $6,000 annually, or $500 per month.

3. Homeowners Insurance (and Possible Hazard Riders)

Your annual homeowners insurance cost depends heavily on your location, its risk of natural disasters, your claims history, and your insurance coverage level.

On a $400,000 home, premiums might run $1,000–$3,000+ annually; in high-risk zones, such as those prone to floods, fires and tornadoes, it could be much more.

4. HOA/Community Fees

If your home is part of a homeowners association, fees might cover maintenance, landscaping, amenities, etc. Monthly HOA dues range drastically from $25–$500+, depending on amenities.

Some HOAs also impose special assessments which carry a large, one-time cost that homeowners are responsible for paying.

5. Maintenance, Repairs, & Replacement Reserves

A common rule of thumb is to budget 1%–4% of the home’s value annually for maintenance and repairs. This range takes the size, location and age of your home and its major systems into account, since older homes or houses in harsh climates often require more upkeep.

For a $400,000 home, that translates to $4,000–$12,000 per year (or ~$333–$1,000 per month).

This covers both routine upkeep (roof, gutters, HVAC servicing, siding, plumbing) and larger replacements (roof, water heater, major systems).

Here’s a sample cost breakdown for a home that costs $400,000:

The All-in Costs of Selling a Home

Selling a property also comes with costs that reduce your net proceeds. Here’s a more detailed breakdown of what you can expect to budget for a home sale.

Common Home Sale Expenses

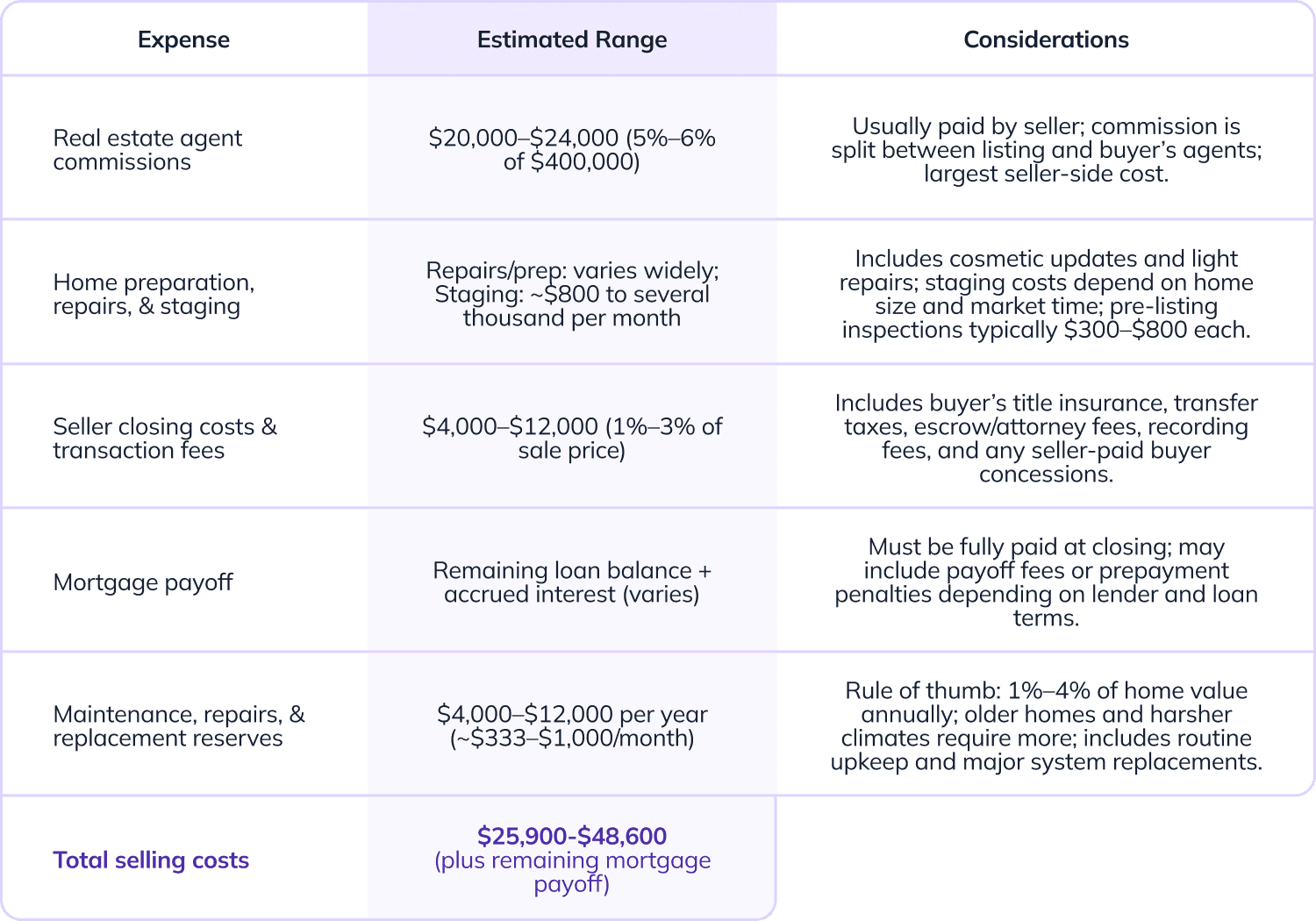

1. Real Estate Agent Commissions

Sellers often pay commissions, typically 5%–6% of the sale price, which are split between the listing and buyer’s agents.

For a $400,000 home, commission alone might be $20,000–$24,000.

2. Home Preparation, Repairs, & Staging

Sellers often invest in cosmetic improvements (e.g., painting, landscaping, light repairs) or more significant upgrades to get their home market-ready and maximize its value.

Staging (renting furniture and decor) might cost anywhere from $800 to several thousand dollars per each month that the home is on the market.

Pre-listing inspections, such as roof, structural, and termite inspections, could cost $300–$800 a piece, but can help reduce buyer renegotiation risk and concessions.

3. Seller Closing Costs & Transaction Fees

These include the buyer’s title insurance, transfer taxes, escrow and attorney fees, recording fees, and any buyer closing cost contributions from the seller.

Seller closing and transaction fees often run 1%–3% of the sale price.

4. Mortgage Payoff

Any remaining mortgage principal (plus accrued interest up to closing) must be paid off before a home sale is finalized. There could be additional prepayment penalties or payoff fees to consider as well.

Here’s a sample cost breakdown for the sale of a $400,000 home:

Tips for Managing Home Buying and Selling Costs

- Budget conservatively: When estimating, err on the high end for repairs, inspections, closing, and moving costs so you have a buffer.

- Negotiate fees when possible: Some real estate commissions, inspection fees, and closing-related costs may be negotiable.

- Shop multiple providers: Get quotes from several inspectors, title insurers, movers, contractors, and staging companies.

- Use seller concessions strategically: In some cases, you might negotiate for the seller to pay part or all of your closing costs (depending on your loan program).

- Time your transaction: In a seller’s market, selling before you buy might yield more leverage; in a buyer’s market, buying first might help you lock in more favorable terms.

- Plan for long-term costs: Don’t discount the impact of increased property taxes, insurance hikes, energy upgrades, or deferred maintenance in your affordability modeling.

Navigating Buying and Selling Simultaneously

One of the trickiest financial challenges is buying your next home while still owning (or trying to sell) your current one. You may face overlapping mortgages, timing constraints, and liquidity limits. Below are some strategies and tools to make that transition smoother.

The Problem of Overlap

When buying and selling at the same time, you may:

- Need to temporarily carry two mortgage payments

- Lack the cash for a down payment if your current home hasn’t sold yet

- Be forced to make contingent offers (e.g., your new offer is contingent on the sale of your old home) which can be less attractive to sellers

- Face a timing gap (closing on your new home before selling the current one), which can complicate the moving process

How Bridge Loans Can Help

A bridge loan is a short-term financing solution that helps you “bridge” the gap between the purchase of your new home and the sale of your current one.

This option allows you to access equity from your current home (or borrow against its value) to fund a down payment on a new home — or temporarily pay off your existing mortgage.

Terms are typically short — spanning 3 to 12 months — and interest rates and fees are higher than conventional mortgages; bridge loan interest rates often range from 10% to 12%+. Plus, closing and origination fees may add 1%–3% of the loan amount.

Many lenders require that you put your current home on the market and that you have an exit plan or payoff strategy (e.g. sale of your old home) before they’ll approve a bridge loan.

How Home Equity Investments Can Help

A home equity investment can be a great alternative to a bridge loan for funding a move. You receive a percentage of your equity in a lump sum of cash to use as a down payment or liquidity. There are no monthly payments owed to the investor for the life of the investment.

When you’re ready to settle the investment — via refinance, savings, loan, or home sale, the investor receives a percentage of the home’s value at that time. Since some home equity investors, including Hometap, offer tiered pricing, the share the investor receives can be less in years 1-3, for example, making a shorter-term investment cost less for the homeowner than an investment spanning 6-10 years. A Hometap Investment, specifically, also features a 20% cap that is designed to protect your interest in your property — and limits the Hometap Share to an annualized 20% rate of return on the original Investment amount, prorated to the date of settlement.

When buying or selling a home, look at the bigger picture beyond the listing price. Costs add up quickly — whether they’re for inspections, appraisals, closing, moving, commissions, taxes, insurance, or repairs. By incorporating buffers and estimating conservatively, you can avoid unpleasant surprises.

You should know

We do our best to make sure that the information in this post is as accurate as possible as of the date it is published, but things change quickly sometimes. Hometap does not endorse or monitor any linked websites. Individual situations differ, so consult your own finance, tax or legal professional to determine what makes sense for you.

Related Tags:

Buying & selling, Home maintenance, Property tax, Home appraisal, Private mortgage insuranceMore in “Financial goals”

Selling Your Home? Get Top Dollar by Tackling These Renovations First

3 Things You Should Do Before You List Your Home for Sale